Carbon Removal

Reading the CDR cost curves

What happens to removal at 2¢ electricity

By Keri Waters ·

When Nan Ransohoff set up Frontier in early 2022, she had to answer a question every CDR buyer has to answer and most get wrong. She had close to a billion dollars in advance market commitments from Stripe, Alphabet, Meta, Shopify, McKinsey, and a handful of others. She had a published cost table. The table told her, in clean rows and columns, what each method of removing CO₂ from the atmosphere cost per ton today. Cheapest at the top. Most expensive at the bottom.

She allocated almost none of the money to the cheap methods.

The analyst-conventional response to that decision would have weighted the buy toward the methods with the best current economics: afforestation, biochar, soil carbon. Frontier went the other direction. The dollars landed on enhanced rock weathering, mineralization, ocean alkalinity, and direct air capture. The $/ton numbers ranged from uncomfortably expensive to openly absurd. When Frontier signed Lithos Carbon in December 2023 for $57.1 million across 154,240 tons of weathered basalt, the implied price was $370 a ton, roughly thirty times the going rate for verified nature-based credits. Earlier purchases from Climeworks had run $775 a ton.

Anyone reading the published cost table would have called Frontier’s portfolio a mistake. They would have been wrong. Frontier was reading a different table.

Every published CDR cost ranking shares one assumption that becomes obvious the moment you state it: the prices are quoted at today’s electricity prices. The IEA technology range, CDR.fyi’s leaderboard, every analyst spreadsheet ordering methods from cheap to expensive. They all rest on a kilowatt-hour cost that was true in 2023 and that nobody serious believes will hold for the next fifteen years. Clean electricity has fallen 90 percent in a decade. Microsoft, Google, Amazon, and Meta are spending north of $600 billion in 2026 on energy-adjacent infrastructure, much of it pulling solar and advanced nuclear down their learning curves. The structural force pushing wholesale electricity toward two cents a kilowatt-hour in solar-rich regions in the 2030s runs on hyperscaler arms-race economics, which are not slowing down.

The table, today and at cheap power

Here are the seven major CDR methods, with their current cost ranges and their cheap-energy cost ranges. Numbers are sourced from CDR.fyi, Frontier’s published agreements, IEA’s CDR roadmap, and direct disclosures from the named companies.

| Method | Today ($/tCO₂) | At 2¢/kWh ($/tCO₂) | Scale potential (Gt/yr) | Energy-intensive |

|---|---|---|---|---|

| Direct Air Capture | $400–1,000 | $80–200 | 20 | Yes |

| Enhanced Rock Weathering | $200–500 | $150–400 | 4 | No |

| Biomass Burial | $100–250 | $80–200 | 3 | No |

| Biochar | $100–300 | $90–250 | 2 | No |

| Ocean Alkalinity (electrochemical) | $150–500 | $100–350 | 10 | Yes |

| Nature-Based | $15–100 | $15–100 | 5 | No |

| Mineralization (DAC-coupled) | $100–300 | $60–200 | 8 | Yes |

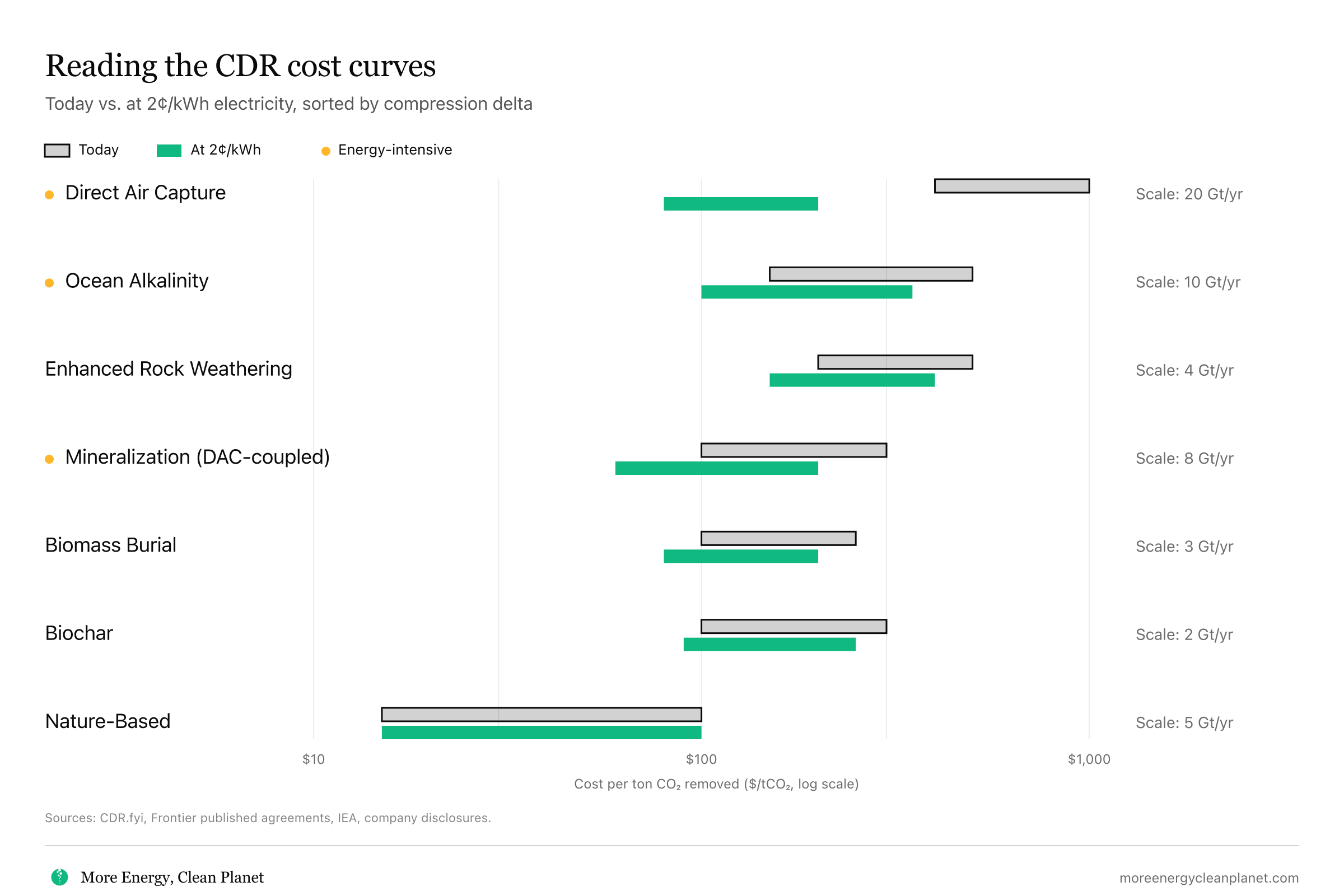

Range-bar chart of seven carbon removal methods showing cost per ton today vs. at 2¢/kWh electricity, sorted by how much each method compresses. Direct air capture shows the largest compression, $400–1,000 today to $80–200 at cheap electricity. Nature-based methods hold at $15–100 in both because electricity is not the binding input. Energy-intensive methods (DAC, Ocean Alkalinity, Mineralization) are marked with an amber dot.

{kind=link}

{kind=link}

Redraw the cost table at the electricity price the hyperscalers are already signing PPAs against in some geographies, and the rankings invert.

The split runs along a clean thermodynamic line. Three methods spend most of their budget on electrons. Four don’t.

Direct air capture spends 40 to 70 percent of its unit cost regenerating sorbent: cycling the bed to 80 or 120 degrees Celsius to release the CO₂ it just pulled from a 420-ppm stream. The thermodynamic minimum for separating a dilute gas runs high; the engineering reality runs higher. Climeworks operates banks of fans drawing air through amine-loaded contactors at its Mammoth facility in Iceland. Heirloom heats limestone in modular reactors in California. CarbonCapture Inc. is shipping DAC modules off an assembly line in Mesa, Arizona. Every one of them carries the same cost stack, dominated by the kilowatt-hours that drive regeneration. Electrochemical ocean alkalinity (Ebb Carbon, Captura) spends most of its budget on the kiloamp direct current that splits seawater into acid and base. DAC-coupled mineralization (44.01 in Oman, Heirloom paired with concrete partners) carries the DAC energy load on its front end and grinding or geological injection on its back. In each case, the bill is the electrons.

The other four methods carry electricity as a marginal line item. Enhanced rock weathering grinds basalt or olivine and trucks it to farmland. The cost stack is logistics: mining, grinding, transport, soil sampling for verification. Mary Yap and her team at Lithos drove their costs down 26 percent in 2025, almost entirely through MRV maturation: faster soil sampling, tighter geochemical models, better satellite confirmation of application. Cheap electricity barely shows up on a weathering ledger. Biomass burial works the same way. Charm Industrial converts agricultural residue into bio-oil and injects it underground; Graphyte presses biomass into dense blocks and stores them in monitored sites. The constraint is feedstock acquisition, not the kilowatt-hours to process it. Biochar pyrolyzes agricultural residue once, mostly self-fueled from the biomass itself; unit cost is dominated by facility capital and soil-application MRV. Nature-based methods run on photons direct from the source.

Cut electricity from ten cents to two and watch what happens. Direct air capture moves from $400-1,000 a ton down to $80-200. Mineralization drops from $100-300 to $60-200. Ocean alkalinity falls from $150-500 to $100-350. Enhanced rock weathering shifts from $200-500 to $150-400, with most of that compression coming from MRV and logistics learning rather than cheaper kilowatt-hours. Biomass burial, biochar, and nature-based hold roughly where they sit. The methods that look most expensive at 2024 electricity prices are the ones that compress most under the conditions the manufactured energy buildout is already producing. The methods that look cheapest today largely hold.

The deeper reason any of this matters has to do with scale.

Nature-based removal caps out around 5 Gt/yr globally before it competes with food production or fails additionality tests. Biochar tops near 2. Biomass burial, 3. Enhanced rock weathering, 4 within a defensible cost envelope. The entire non-energy-intensive portfolio sums to roughly 14 Gt/yr at maximum stretch.

The hundred-year repair requires 15 to 30 Gt/yr of removal by the 2060s to bring atmospheric CO₂ back to pre-industrial concentrations within a century. Anything below 14 Gt/yr produces a slower atmosphere, decades behind the math. Reaching 15 to 30 requires the energy-intensive methods at scale. DAC carries 20+ Gt/yr of physical headroom by IEA estimates. Ocean alkalinity, 10. Mineralization, 8. Together they cover the gap. Separately, the methods that scale to the atmosphere are exactly the methods whose unit economics collapse to viability when electricity gets cheap.

Frontier was buying tons at $370 and $775 because Ransohoff was placing a forward bet on what the cost table would read in 2040, not what it read on the day she signed the check. Every AMC dollar deployed against an expensive method today buys deployment learning, manufacturing scale, and operational maturity that bends the cost curve down. Her buyers were paying tuition on Wright’s law, applied to atmospheric repair.

Of the three energy-intensive methods, direct air capture is the largest single lever. The case is mechanical. DAC has the largest energy share of unit cost, which produces the steepest compression as electricity falls. It has the largest physical headroom, more than 20 Gt/yr. Its current cost runs the highest, which leaves its learning curve the most room to run. And its tons are the most legible in the portfolio: meter the gas at the inlet, meter what gets stored, the gap is the removal. No reversal risk, no permanence discount, no soil-chemistry uncertainty.

Klaus Lackner at Arizona State has been arguing for direct air capture since 1999, when his proposed costs were considered laughable and his research program was a curiosity at the edge of the field. The chemistry was always sound. The energy economics were never going to be sound under the grid he was talking to. They are becoming sound under a grid paying for itself with AI compute revenue, which Lackner did not predict and which nobody had to predict for the cost curve to bend.

Wright’s law pulled solar from $7.34 a watt in 2010 to under $1 a watt by 2024. It pulled lithium-ion batteries down roughly 90 percent over the same period. It is now pulling advanced fission down its own curve as Radiant, Oklo, and Aalo compete to ship reactors off assembly lines instead of pouring them as construction projects. Direct air capture sits roughly where solar sat in 2010, with the chemistry already solved and the cost reduction running through manufacturing and deployment learning. Heirloom, Climeworks, CarbonCapture, and 1PointFive are paying tuition on that curve right now. Every plant they ship is a unit on the learning curve. Every offtake agreement signed by Microsoft, Google, or Frontier funds another increment of the descent.

A dollar spent pulling DAC down its cost curve in 2026 buys vastly more 2040 tons than the same dollar spent on cheap nature-based credits in 2026. Cheap tons are real, verifiable, and worth buying for what they are. The scale that closes the atmospheric math lives inside the methods whose costs only work at cheap-power prices.

Continue at /sectors/carbon-removal → for the companies, indicators, and ongoing analysis behind the pillar.